專業叢書

(2026最新版本)美國報稅與海外財產揭露─美國信託、跨境資產傳承

附錄

附錄六:3520表(境外信託及贈與申報表)及其申報說明

3520表申報說明

為兼顧版面精簡和實用性,編者刪去第一和第二部分,保留第三和第四部分供讀者參考。

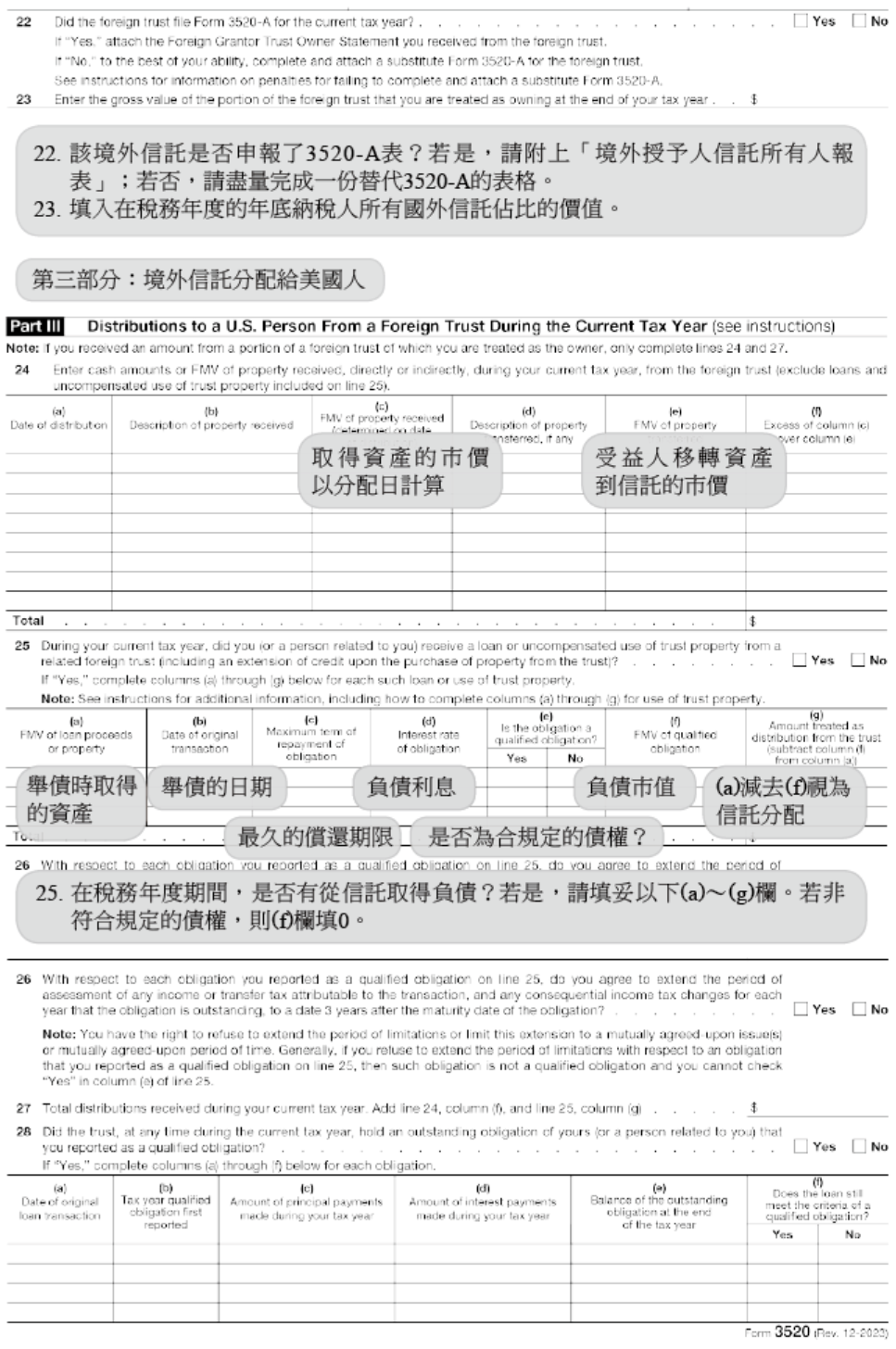

第三部分──在現行稅務年度中,從境外信託分配給美國人

Part III—Distributions to a U.S. Person From a Foreign Trust During the Current Tax Year

如果您從境外信託的一部分收到一筆款項,而又被視為這個境外信託的擁有人,請填寫第三部分的 24 和 27 行。如果您從境外信託收到一筆款項,而這筆款項需要在 3520 表的第三和第四部分進行申報,那麼請您只在第三部分申報這筆款項。

If you received an amount from a portion of a foreign trust of which you are treated as the owner, complete lines 24 and 27 in Part III. If you received an amount from a foreign trust that would require a report under both Parts III and IV (gifts or bequests) of Form 3520, report the amount only in Part III.

第 24 行

請申報在現行稅務年度當中,您從境外信託中收到的任何現金或其他資產(實際或推定,直接或間接),不論課說與否,除非該筆款項是從信託提供您的貸款,或構成對信託財產的無償使用。否則務必要在第 25 行申報。例如,如果您是一個合夥組織的合夥人,而從境外信託中獲得分配,那麼請務必要申報該款項中屬於您的可分配的股份,作為來自這個信託的間接分配。

Report any cash or the FMV of other property that you received (actually or constructively, directly or indirectly) from a foreign trust during the current tax year, whether or not taxable, unless the amount is a loan to you from the trust or constitutes uncompensated use of trust property, both of which must be reported on line 25. For example, if you are a partner in a partnership that receives a distribution from a foreign trust, you must report your allocable share of such payment as an indirect distribution from the trust.

第 24 行 (c) 欄

如果受益人手中資產的基準(如同 643(e)(1) 條款規定)低於資產的市價,則允許申報人填入該資產的基準;但只有在納稅義務人因缺乏憑證而不需要完成附表 A(第 31~38 行)的情況下可這樣做。

因為這樣的緣故,缺乏憑證會關係到申報者在第 29 或 30 行勾選「否」,因為:(a) 受益人並沒有從信託收到《外國授予人信託受益人申報書》或《外國非授予人信託受益人申報書》,或 (b) 這樣的申報表並沒有包括這份說明下面第 29 行或第 30 行所有的特定項目。

The filer is permitted to enter the basis of the property in the hands of the beneficiary (as determined under section 643(e)(1)), if lower than the FMV of the property, but only if the taxpayer is not required to complete Schedule A (lines 31 through 38) due to lack of documentation. For these purposes, lack of documentation refers to a situation in which the filer checked “No” on line 29 or 30 because (a) the beneficiary did not receive a Foreign Grantor Trust Beneficiary Statement or a Foreign Nongrantor Trust Beneficiary Statement from the trust, or (b) such statement did not contain all of the items specified under the instructions for line 29 or 30, later.

第 25 行

如果您或是與您有關係的美國個人,直接或間接,從一個相關的境外信託收到現金借款或是有價證券的借款,或無償使用信託財產(定義見下文),此借貸的金額或使用信託財產的FMV將被視為應申報的分配,無論是否應納稅。為了這個緣故,由境外信託擔保的非相關的第三方提供您的貸款,通常會被視為來自信託的貸款。

If you or a U.S. person related to you received a loan of cash or marketable securities, directly or indirectly, from a related foreign trust, or the uncompensated use of trust property (defined later), the amount of such loan or the FMV of the use of trust property will be treated as a reportable distribution, whether or not taxable. For this purpose, a loan to you by an unrelated third party that is guaranteed by a foreign trust is generally treated as a loan from the trust.

第 25 行 (e) 欄

如果您被給予的債權用來交換貸款,是一項符合規定的債權(見稍早定義),請回答「是」。

Answer “Yes” if your obligation given in exchange for the loan is a qualified obligation (defined earlier).

第 25 行 (f) 欄

除非是符合規定的債權,否則該債權的市價為 0。因此,在是合規定債權的情況下,請在 (f) 欄中填入「-0-」。

The FMV of an obligation is zero unless it is a qualified obligation. Therefore, in the case of obligations that are not qualified obligations, enter “-0-” in column (f).

信託資產的無償使用/Uncompensated use of trust property

如果您或是與您有關係的美國個人,直接或間接,使用境外信託的任何資產,則此類使用權的市價,將被視為可申報的分配,無論是否應納稅。請在 (a) 欄申報信託資產未補償使用的市價,並且在 (b) 欄申報第一次使用的日期;請跳過 (c)~(e) 欄,在 (f) 欄申報為此類用途所支付的金額,以及從 (a) 欄減去 (f) 欄,在 (g) 欄中輸入被視為來自信託的應稅分配的金額。相關詳細資訊請參閱第 643(i) 條。

If you or a U.S. person related to you, directly or indirectly, used any property of a foreign trust, the FMV of such use will be treated as a reportable distribution whether or not taxable. Report the FMV of the use of trust property in column (a) and the date of first use in column (b), skip columns (c) through (e), report the amount paid for such use in column (f), and enter the amount treated as a taxable distribution from the trust in column (g) by subtracting column (f) from column (a). See section 643(i) for more information.

註:根據 2010 年 3 月 18 日之後生效的《美國投資法案》,如果一個有美國轉讓人的外國信託沒有根據第 671 至 679 條的規則被視為贈與人信託,那麼,如果該外國信託直接或間接向美國人提供現金或有價證券的貸款,或允許美國人直接或間接使用信託財產,而美國人沒有按市場利率償還貸款或向信託公司支付信託財產的FMV,則該外國信託將被視作授予人信託。如果它直接或間接向美國人提供現金或有價證券貸款,或允許美國人直接或間接使用信託財產,而該美國人沒有在合理的時間內以市場利率償還貸款或向信託公司支付使用該財產的 FMV。因此,根據第 643(i) 條,貸款或使用信託資產將不被視為應稅分配,但仍需在本 3520 表的第三部分報告。

Under the HIRE Act, effective after March 18, 2010, if a foreign trust with a U.S. transferor is not already treated as a grantor trust under the rules of sections 671 through 679, the foreign trust will be treated as having acquired a U.S. beneficiary, and will therefore be treated as a grantor trust, if it makes a loan of cash or marketable securities, directly or indirectly, to a U.S. person or allows a U.S. person, directly or indirectly, to use trust property, and the U.S. person does not repay the loan at a market rate of interest or pay the trust the FMV of the use of the property within a reasonable period of time. Accordingly, the loan or use of trust property will not be treated as a taxable distribution under section 643(i) but will remain reportable on Part III of this Form 3520.

第 28 行

請提供境外信託的未償付債權的狀態資訊,而這些未償付債權是您在現行年度中申報為符合規定的債權的。這些資訊是用來將這些債權保留在合規定債權的狀態。必要的話,請您附加一份報表來描述這項合規定債權中的任何條件改變。如果這項債權未能保留在合規定債權的狀態,您將按照第 643(i) 條被視為已經從境外信託收到應稅分配。請見 97-34 聲明的 V(A) 條款。

Provide information on the status of any outstanding obligation to the foreign trust that you reported as a qualified obligation in the current tax year. This information is required in order to retain the obligation’s status as a qualified obligation. If relevant, attach a statement describing any changes to the terms of the qualified obligation. If the obligation fails to retain the status of a qualified obligation, you will be treated as having received a taxable distribution under section 643(i) from the foreign trust. See section V.A. of Notice 97-34.

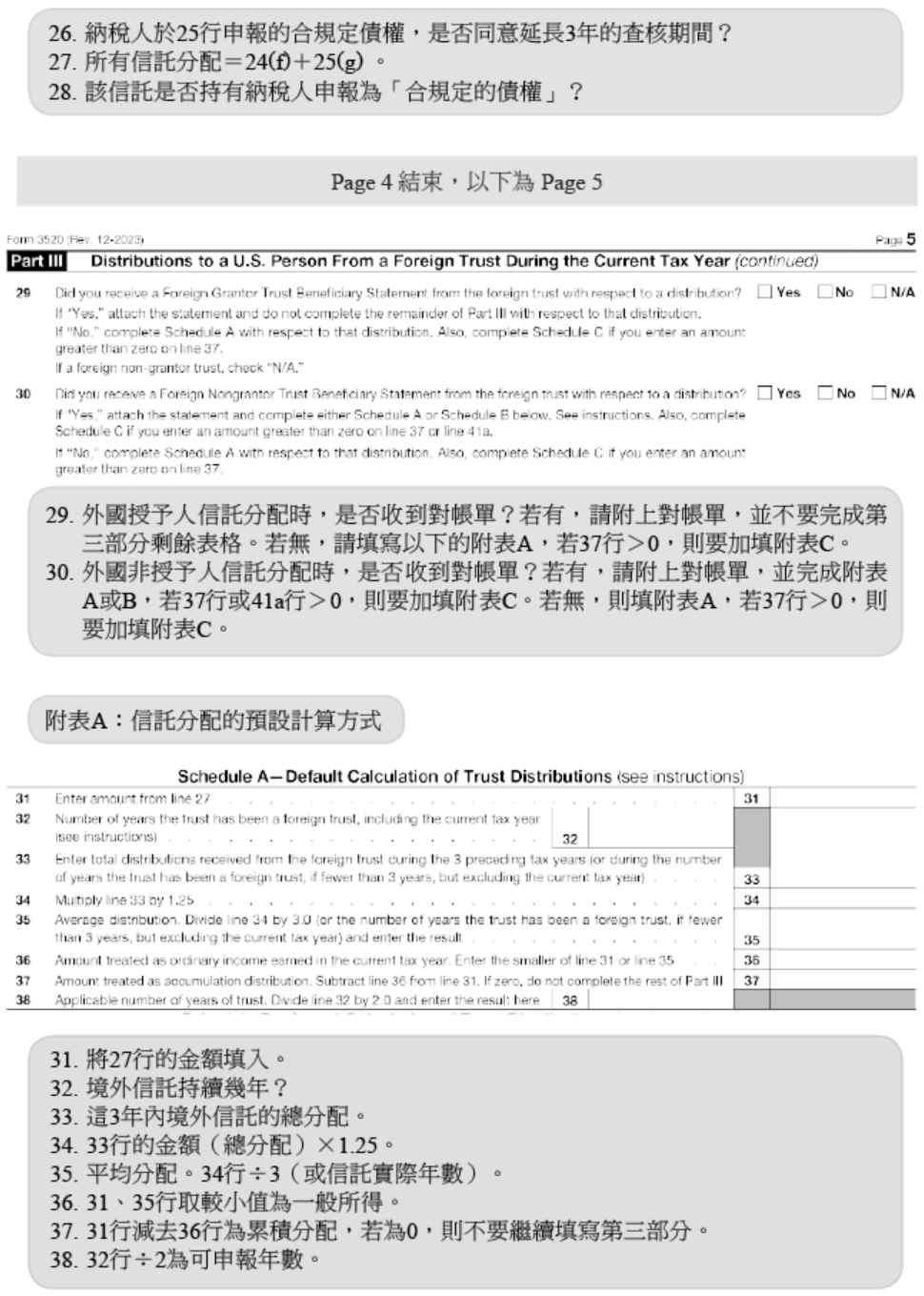

第 29 行

若您因分配而收到外國設立者信託受益人聲明(3520-A 表第 5頁),請勾選「是」。請附上外國信託提供的受益人聲明,且無須就該分配完成第三部分的其餘部分。

Check “Yes” if you received a Foreign Grantor Trust Beneficiary Statement (page 5 of Form 3520-A) from the foreign trust with respect to a distribution. Attach the Foreign Grantor Trust Beneficiary Statement from the foreign trust and do not complete the rest of Part III with respect to the distribution.

如果美國受益人在稅務年度中,就某筆分配收到完整的《外國授予人信託受益人申報書》,則該受益人於所得稅目的下,應將該筆分配視同直接來自信託所有人。例如,若該分配屬於贈與,受益人即無須將該分配計入總所得。

If a U.S. beneficiary receives a complete Foreign Grantor Trust Beneficiary Statement with respect to a distribution during the tax year, the beneficiary should treat the distribution for income tax purposes as if it came directly from the owner. For example, if the distribution is a gift, the beneficiary should not include the distribution in gross income.

除了這個境外信託和其受託人的基本資料(例如名字、地址、TIN 等等)之外,這份申報書務必包括下列項目:

In addition to basic identifying information (see Identifying Information, earlier) about the foreign trust and its trustee, this statement must contain these items.

1. 這份申報書在稅務年度當中,適用於該境外信託的第一天和最後一天。

The first and last day of the tax year of the foreign trust to which this statement applies.

2. 必要的解釋,用來說明及證實為了申報美國所得稅,這個境外信託應被視為由另一個人所擁有。此項解釋必須指出是依照哪一個條款所認定的。

An explanation of the facts necessary to establish that the foreign trust should be treated for U.S. tax purposes as owned by another person. The explanation should identify the Code section that treats the trust as owned by another person.

3. 一份聲明書,用來說明信託的所有人為個人、公司或合夥組織。

A statement identifying whether the owner of the trust is an individual, trust, corporation, or partnership.

4. 對於資產的描述(包括現金部分)。這些資產在稅務年度當中,依照資產的市價分配或被視為分配給美國個人。

A description of property (including cash) distributed or deemed distributed to the U.S. person during the tax year, and the FMV of the property distributed.

5. 一份聲明書,聲明該信託將許可美國國稅局或是美國受益人,審查或備份該信託的永久會計帳簿、紀錄,以及其他的文件,用來證實該信託為了申報美國所得稅,因此應被視為被另外一個人所擁有。但如果該信託已經任命了美國代理人,那麼就不需要出示這份聲明書。

A statement that the trust will permit either the IRS or the U.S. beneficiary to inspect and copy the trust’s permanent books of account, records, and such other documents that are necessary to establish that the trust should be treated for U.S. tax purposes as owned by another person. This statement is not necessary if the trust has appointed a U.S. agent.

6. 一份聲明書,聲明這個境外信託是否任命了美國代理人(見稍早定義)。如果這個信託有美國代理人,請在聲明書當中加入該代理人的名字、地址及納稅人識別號碼。

A statement as to whether the foreign trust has appointed a U.S. agent (defined earlier). If the trust has a U.S. agent, include the name, address, and TIN of the agent.

若《外國授予人信託受益人申報書》中,任何一項應載明的資訊有缺漏,則應視情況於第 29 行或第 30 行勾選勾選「否」。

此外,如果您回答「是」,並且被美國國稅局要求或是傳喚時,境外信託或美國代理人並沒有留下紀錄或證詞,美國國稅局可以重新判定您和該信託之間的交易的稅務結果,並且根據 6677 條款處以適當的罰款。(見 6048(c)(2)(A) 條款)

If any of the items required for the Foreign Grantor Trust Beneficiary Statement is missing, you must check “No” on line 29 or line 30, as applicable.

Also, if you answer “Yes” and the foreign trust or U.S. agent does not produce records or testimony when requested or summoned by the IRS, the IRS may redetermine the tax consequences of your transactions with the trust and impose appropriate penalties under section 6677. See section 6048(c)(2)(A).

第 30 行

若您就某筆分配收到《外國非授予人信託受益人申報書》,請勾選「是」。請附上外國信託提供的《外國非授予人信託受益人申報書》,內容必須包含下列項目:

Check “Yes” if you received a Foreign Nongrantor Trust Beneficiary Statement from the foreign trust with respect to a distribution. Attach the Foreign Nongrantor Trust Beneficiary Statement from the foreign trust. A Foreign Nongrantor Trust Beneficiary Statement must include the following items.

1. 請解釋為了申報美國稅而做的任何分配或視為分配為適當處理,或是提供充分的資訊,可以證實美國受益人是為了申報美國稅,做出任何分配或視為分配的適當處理。

An explanation of the appropriate U.S. tax treatment of any distribution or deemed distribution for U.S. tax purposes or sufficient information to enable the U.S. beneficiary to establish the appropriate treatment of any distribution or deemed distribution for U.S. tax purposes.

2. 一份聲明書,用來說明任何一位信託授予人是否為合夥組織或是外國公司。如果是的話,請附上相關事實的解釋。

A statement identifying whether any grantor of the trust is a partnership or a foreign corporation. If so, attach an explanation of the relevant facts.

3. 一份聲明書,聲明該信託將許可美國國稅局或美國受益人,審查並且備份該信託的永久會計帳簿、紀錄,以及其他文件,用來證實為了申報美國稅,任何分配或視為分配是適當處理。但如果該信託已經任命了美國代理人,那麼就不需要出示這份聲明書。

A statement that the trust will permit either the IRS or the U.S. beneficiary to inspect and copy the trust’s permanent books of account, records, and such other documents that are necessary to establish the appropriate treatment of any distribution or deemed distribution for U.S. tax purposes. This statement is not necessary if the trust has appointed a U.S. agent.

4. 《外國非授予人信託受益人申報書》也務必包括了第一、第四和第六個項目(如同第 29 行的申報說明中所列),以及關於該境外信託及其受託人的基本資料(例如名字、地址及 TIN 等等)。

The Foreign Nongrantor Trust Beneficiary Statement must also include items (1), (4), and (6), as listed in the line 29 instructions, earlier, in addition to the basic identifying information (see Identifying Information, earlier) about the foreign trust and its trustee.

附表A──信託分配的預設計算方式

Schedule A—Default Calculation of Trust Distributions

如果您在第 30 行回答「是」,您就會要填寫附表 A 或 B。然而,一般而言,如果您在當年度填寫附表 A,或是在先前的年度填寫附表 A),在未來的所有年度都要填寫該附表,即便您在未來的某個年度,在第 30 行能夠回答「是」。這項一致性規定的唯一例外是,您可以在一個信託終止的年度使用附表 B,但只有在終止的那一個年度,您可以在第 30 行回答「是」。

If you answered “Yes” to line 30, you may complete either Schedule A or Schedule B. Generally, if you complete Schedule A in the current year, or did so in the prior years, you must continue to complete Schedule A for all future years, even if you are able to answer “Yes” to line 30 in that future year. The only exception to this consistency rule is that you may use Schedule B in the year that a trust terminates, but only if you are able to answer “Yes” to line 30 in the year of termination.

第 32 行

請您在所知的範圍之內,指出信託存在為境外信託的年數,並且附上一份解釋基準。只要信託存在的任何一年,都要算為完整的一個年度。如果這是該信託成為境外信託的第一年,請不要填寫剩下的第三部分。

To the best of your knowledge, state the number of years the trust has been in existence as a foreign trust and attach an explanation of your basis for this statement. Consider any portion of a year to be a complete year. If this is the first year that the trust has been a foreign trust, do not complete the rest of Part III.

第 33 行

請填入在先前三個稅務年度(若成為境外信託少於 3 年,則按實際情況填寫),您所收到的分配總額。舉例來說,如果一個信託在第一年分配 50 美元,第二年分配 120 美元,以及第三年分配 150 美元,那麼在第 33 行申報的總額為 320 美元($50+$120+$150)。

Enter the total amount of distributions that you received during the 3 preceding tax years (or the number of years the trust has been a foreign trust if fewer than 3 years). For example, if a trust distributed $50 in year 1, $120 in year 2, and $150 in year 3, the amount reported on line 33 would be $320 ($50 + $120 + $150).

第 35 行

請把第 34 行的數字除以 3.0(若少於 3 年,就是除以該信託成為境外信託的年數)。只要信託存在的任何一年,都要算為完整的一個年度。例如,一個在 2021 年 7 月 1 日設立的境外信託,會在 2023曆年制的申報書上,被視為有二個先前年度(2021 和 2022 年)。在這個例子中,您把第 34 行的總額除以 2.0,就是第 35 行的總額。請不要忽略沒有進行分配的稅務年度。美國國稅局將會視您的這些先前分配的證明為適當的紀錄,用來說明加總為第 31 行的任何分配,不是在現行稅務年度中的累積分配。

Divide line 34 by 3.0 or the number of years the trust has been a foreign trust if fewer than 3 years. Consider any portion of a year to be a complete year. For example, a foreign trust created on July 1, 2021, would be treated on a 2023 calendar year return as having 2 preceding years (2021 and 2022). In this case, you would calculate the amount on line 35 by dividing line 34 by 2.0. Do not disregard tax years in which no distributions were made. The IRS will consider your proof of these prior distributions as adequate records to demonstrate that any distribution up to the amount on line 31 is not an accumulation distribution in the current tax year.

第 36 行

請填入在您的稅務申報書上作為一般所得的總額。請在您申報書上適合的附表上,申報這個總額(例如 1040 表的附表 E 的第三部分)。

Enter this amount as ordinary income on your income tax return. Report this amount on the appropriate schedule of your tax return (for example, Schedule E (Form 1040), Part III).

第 37 行

如果在第 37 行有金額,請您務必也要完成第 38 行和附表 C「利息費用的計算」,來判定您可能積欠的任何利息費用的總額。

If there is an amount on line 37, you must also complete line 38 and Schedule C — Calculation of Interest Charge to determine the amount of any interest charge you may owe.

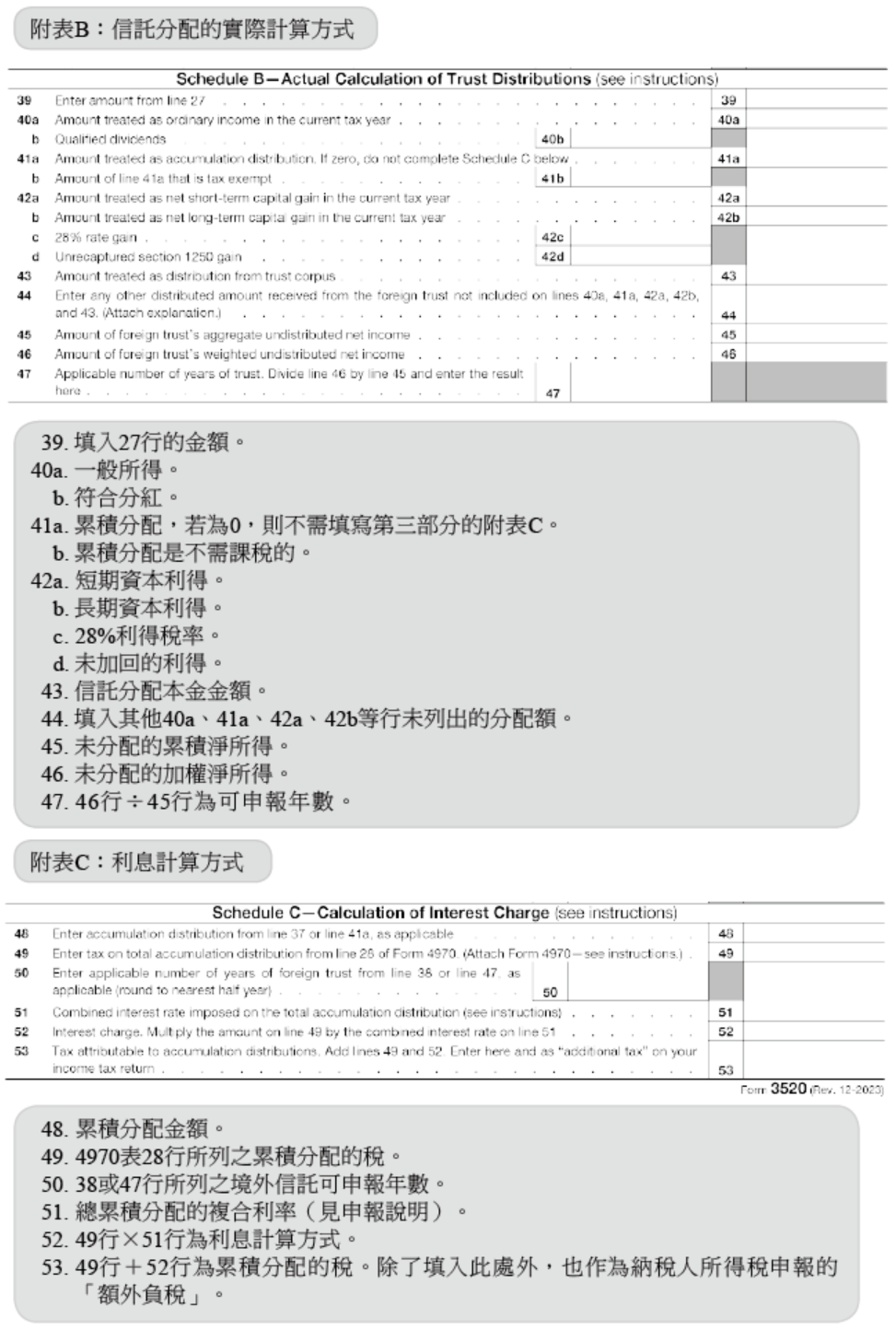

附表B──信託分配的實際計算方式

Schedule B—Actual Calculation of Trust Distributions

只有在下列情況下,您才會使用到附表 B:

You may only use Schedule B if:

- 在第 30 行,您回答「是」。

You answered “Yes” to line 30,

- 您在這份申報書上,附加了一份《外國非授予人信託受益人申報書》的副本,並且

You attach a copy of the Foreign Nongrantor Trust Beneficiary Statement to this return, and

- 您之前不曾因為該境外信託而申報附表 A,或是該境外信託在稅務年度中終止了。

You have never before used Schedule A for this foreign trust or this foreign trust terminated during the tax year.

第 40a 行

請在 40a 行填入您收到來自境外信託的總額,而該總額在現行的稅務年度中被視為信託的一般實際所得。一般實際所得就是非資本利得的所有所得。請在您的稅務申報書的適當的附表中,申報這個總額(例如,1040 表的附表 E 第三部分)。

Enter on line 40a the amount received by you from the foreign trust that is treated as ordinary income of the trust in the current tax year. Ordinary income is all income that is not capital gains. Report this amount on the appropriate schedule of your tax return (for example, Schedule E (Form 1040), Part III).

第 42a~42d 行

請在這幾行中填入可適用的總額,這些總額是您從境外信託收到,並在現行的稅務年度被視為信託的資本利得所得。請在您的所得稅申報書的合適附表上,申報這些總額(例如,1040 表的附表 D)。

Enter on these lines the applicable amounts received by you from the foreign trust that are treated as capital gain income of the trust in the current tax year. Report these amounts on the appropriate schedule of your tax return (for example, Schedule D (Form 1040)).

第 45 行

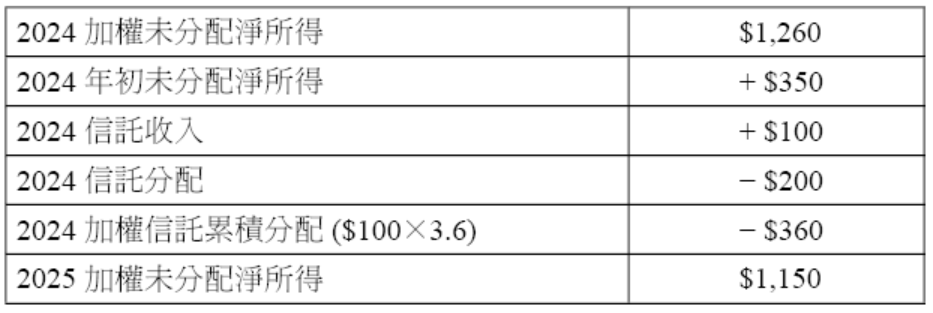

請填入境外信託的加總未分配的淨所得。

舉例。假設信託設立於 2018 年,並且在 2024 年之前都沒有進行分配。假設該信託的一般所得在 2023 年是 0,2022 年是 60 美元,2021 年是 124 美元,2020 年是 87 美元,2019 年是 54 美元,2018 年是 25 美元。因此,針對 2024 年,該信託加總的未分配淨所得會是 350 美元。如果該信託在 2024 年賺了 100 美元,並且分配了 200 美元(以致於當中有 100 美元是從累積收入中進行分配),那麼該信託 2025 年加總的淨所得會是 250 美元($350+$100-$200)。

Enter the foreign trust’s aggregate undistributed net income (UNI). Example. A trust was created in 2018 and has made no distributions prior to 2024. Assume the trust’s ordinary income was $0 in 2023, $60 in 2022, $124 in 2021, $87 in 2020, $54 in 2019, and $25 in 2018. Thus, for 2024, the trust’s UNI would be $350. If the trust earned $100 and distributed $200 during 2024 (so that $100 was distributed from accumulated earnings), the trust’s 2025 aggregate UNI would be $250 ($350 + $100-$200).

第 46 行

請填入境外信託的加權未分配淨所得。信託的加權未分配淨所得就是其累積且還未進行分配的所得,並藉由有累積所得的年度進行加權。為了要計算加權未分配的淨所得,請把來自每一個信託年度的未分配所得,乘上自那一年起的年數,再將每一年的結果合計。以第 45 行的例子來算,信託在 2024 年的加權未分配淨所得是 1,260 美元,計算如下:

Enter the foreign trust’s weighted undistributed net income (weighted UNI). The trust’s weighted UNI is its accumulated income that has not been distributed, weighted by the years that it has accumulated income. To calculate weighted UNI, multiply the undistributed income from each of the trust’s years by the number of years since that year, and then add each trust’s result. Using the example from line 45, the trust’s weighted UNI in 2024 would be $1,260, calculated as follows:

為了要計算接下來年度(2025 年)信託的加權未分配的淨所得,信託可以更新這裡的計算結果,或是顯示在 2024 年 3520 表第 46 行的加權未分配的淨所得,可以藉由下列的步驟更新:

To calculate the trust’s weighted UNI for 2025, the trust could update this calculation, or the weighted UNI shown on line 46 of the 2024 Form 3520 could simply be updated using the following steps.

1. 從 2024 年加權的未分配的淨所得開始。

Begin with the 2024 weighted UNI.

2. 在 2024 年開始時,加上未分配的淨所得。

Add UNI at the beginning of 2024.

3. 加上在 2024 年的信託收入。

Add trust earnings in 2024.

4. 減去在 2024 年的信託分配。

Subtract trust distributions in 2024.

5. 減去 2024 年的加權信託累積分配。(加權信託累積分配就是把 2024 年的信託累積分配,乘上從 2024 年起的可適用年數。)

Subtract weighted trust accumulation distributions in 2024. (Weighted trust accumulation distributions are the trust accumulation distributions in 2024 multiplied by the applicable number of years from 2024.)

以上面的例子來算,這個信託的 2025 年的加權未分配淨所得會是 1,150 美元,計算如下。

Using the example above, the trust’s 2025 weighted UNI would be $1,150, calculated as follows.

第 47 行

把第 46 行的數字除以第 45 行的數字,來計算信託的可適用年數。請使用在申報說明中針對第 45 行和第 46 行的例子,信託的可適用年度在 2024 年是 3.6(1,260/350),而在 2025 年是 4.6(1,150/250)。

Calculate the trust’s applicable number of years by dividing line 46 by line 45. This would be the weighted UNI divided by the annual UNI. Using the examples in the instructions for lines 45 and 46, the trust’s applicable number of years would be 3.6 (1,260/350) in 2024 and 4.6 (1,150/250) in 2025.

註:如果在第 45 行的未分配淨所得的數字中有小數點的話,請不要刪除(例如,請使用在申報說明中第 45 行的例子,保留小數點後面三位數字)。

Note: Include as many decimal places as there are digits in the UNI on line 45 (for example, using the example in the instructions for line 45, include three decimal places).

附表C──利息費用的計算

Schedule C—Calculation of Interest Charge

如果您在第 37 行或第 41a 行有填入金額的話,請完成附表 C。

Complete Schedule C if you entered an amount on line 37 or line 41a.

第 49 行

請把本表第 48 行的金額,納入在 4970 表的第 1 行。然後使用 4970 表第 1~28 行,來計算總累積分配的稅負。請在第 49 行填入來自 4970 表第 28 行的稅負。

Include the amount from line 48 of this form on line 1 of Form 4970, Tax on Accumulation Distribution of Trusts. Then, compute the tax on the total accumulation distribution using lines 1 through 28 of Form 4970. Enter on line 49 the tax from line 28 of Form 4970.

註:請使用 4970 表作為工作附表,並將其附加在 3520 表上。

Note: Use Form 4970 as a worksheet and attach it to Form 3520.

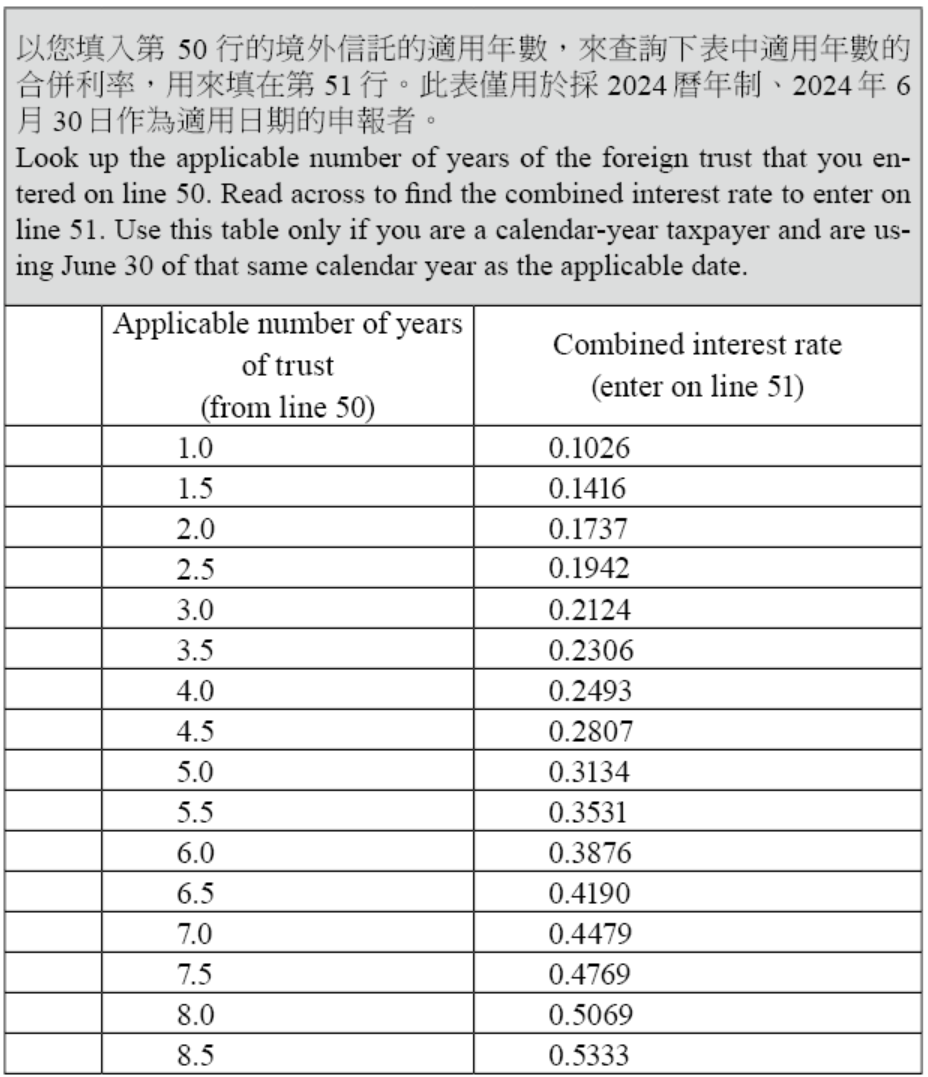

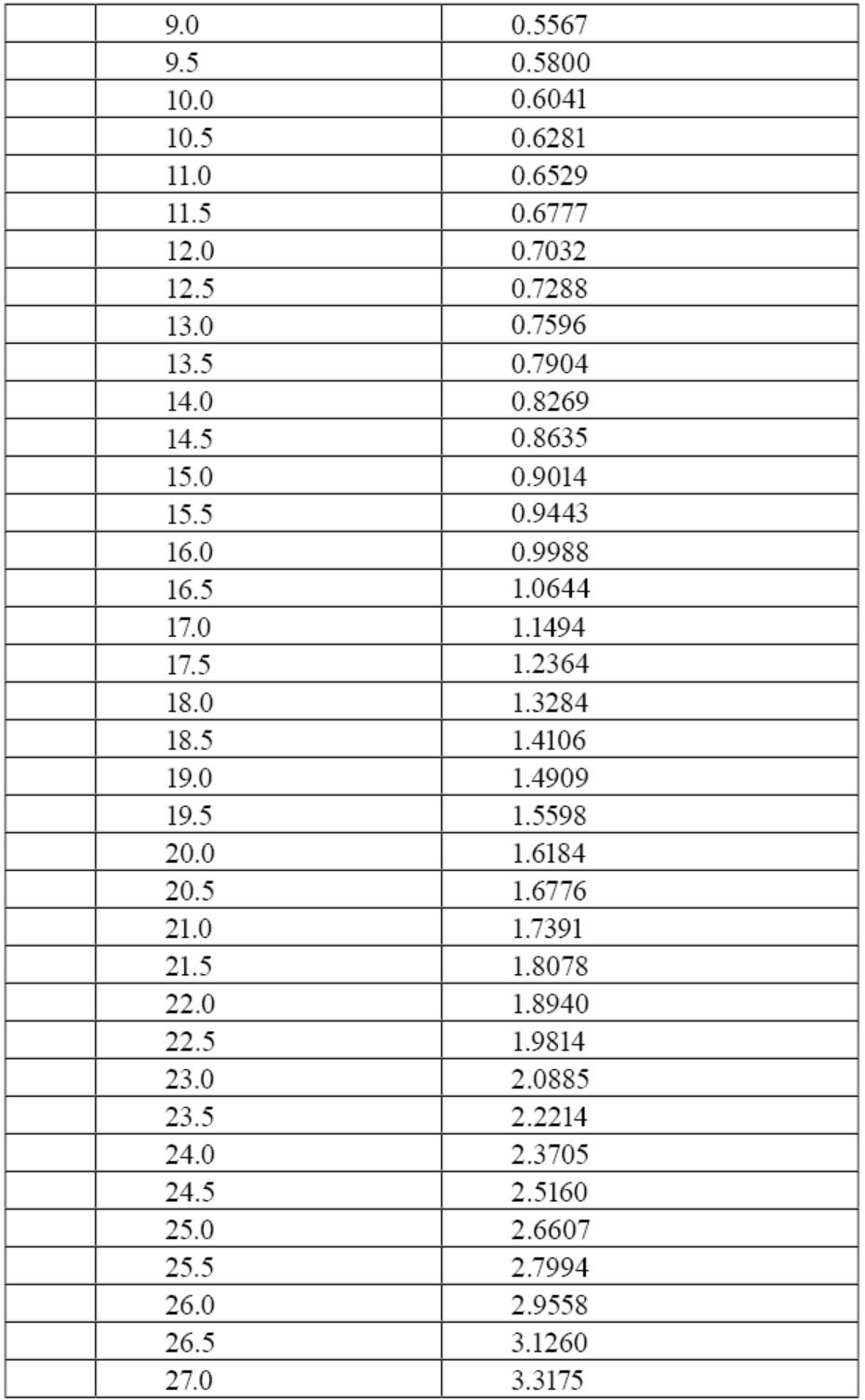

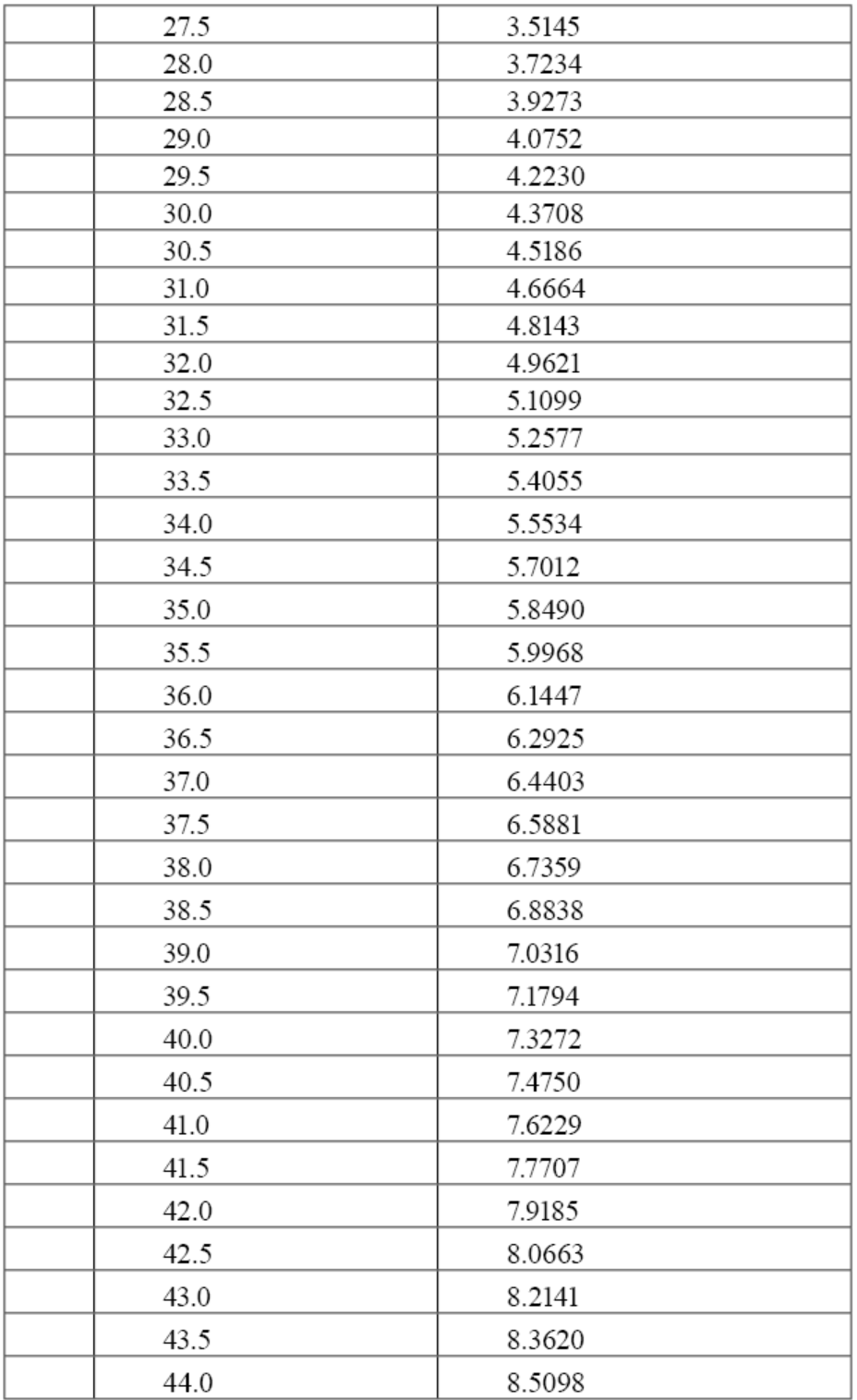

第 51 行

一段期間會有稅負的累積利息(第 49 行),而這段期間是開始於適用日期之前的適用年數中的某一個日期,並結束於適用日期。為了計算利息,適用日期就是進行申報的稅務年度的年中(例如,採用 2025 曆年制,適用日期就是 2025 年 6 月 30日)。

另外一種選擇是,如果您在稅務年度只收到一項累積分配,您可以使用分配的日期作為適用日期。

針對 1996 年之前、1976 年之後的利息累積期間,利息是以每年 6% 的單利來累積,而沒有複利。而 1995 年之後的利息累積期間,則是根據 6621(a)(2) 條款,每日以複利來計算,以課徵不足繳納的稅負。1995 年後這段期間的複利,不只是加徵在稅負上,也加在歸屬於 1996 年前的期間的總單利。

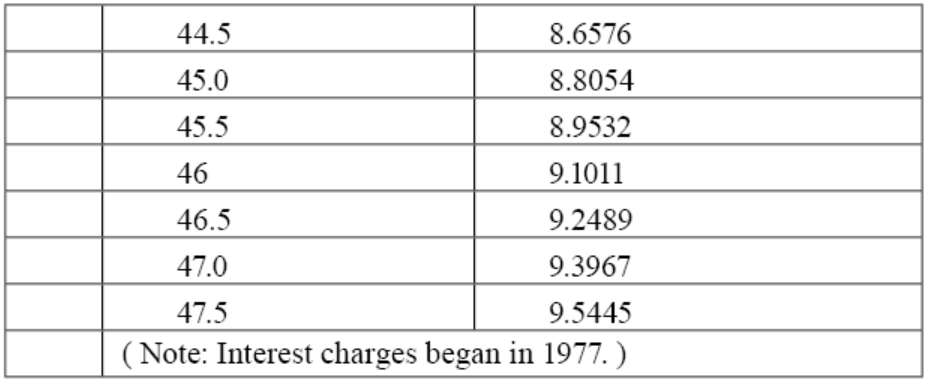

如果您是採用曆年制來申報,並且使用 6 月 30 日作為計算利息的適用日期,請使用下面的表格來決定合併的利率,並請將合併的利率填入 51 行。如果您不是採用曆年制,或您選擇分配的真正日期作為適用日期,請依照上面的原則來計算合併利率,並且將其填入 51 行。

Interest accumulates on the tax (line 49) for the period beginning on the date that is the applicable number of years (as rounded on line 50) prior to the applicable date and ending on the applicable date. For purposes of making this interest calculation, the applicable date is the date that is mid-year through the tax year for which reporting is made. For example, in the case of a 2025 calendar-year taxpayer, the applicable date would be June 30, 2025.

Alternatively, if you received only a single distribution during the tax year that is treated as an accumulation distribution, you may use the date of that distribution as the applicable date.

For portions of the interest accumulation period that are prior to 1996 and after 1976, interest accumulates at a simple rate of 6% annually, without compounding. For portions of the interest accumulation period that are after 1995, interest is compounded daily at the rate imposed on underpayments of tax under section 6621(a)(2). This compounded interest for periods after 1995 is imposed not only on the tax, but also on the total simple interest attributable to pre-1996 periods.

If you are a calendar-year taxpayer and you use June 30 of the calendar year as the applicable date for calculating interest, use the table found on IRS.gov/CombinedInterestRate to determine the combined interest rate and enter it on line 51. If you are not a calendar-year taxpayer or you choose to use the actual date of the distribution as the applicable date, calculate the combined interest rate using the above principles and enter it on line 51.

累積分配總額的合併利率一覽表

Table of Combined Interest Rate Imposed on the Total Accumulation Distribution

第 53 行

請將作為「附加稅(ADT)」的總額,申報在所得稅申報書的適當欄位。(舉例來說,1040 表的申報者請將此金額加在附表 2(1040表)第 17z 行的總額裡)

Report this amount as additional tax (ADT) on the appropriate line of your income tax return (for example, for Form 1040 filers, include this amount as part of the total for line 17z on Schedule 2 (Form 1040)).

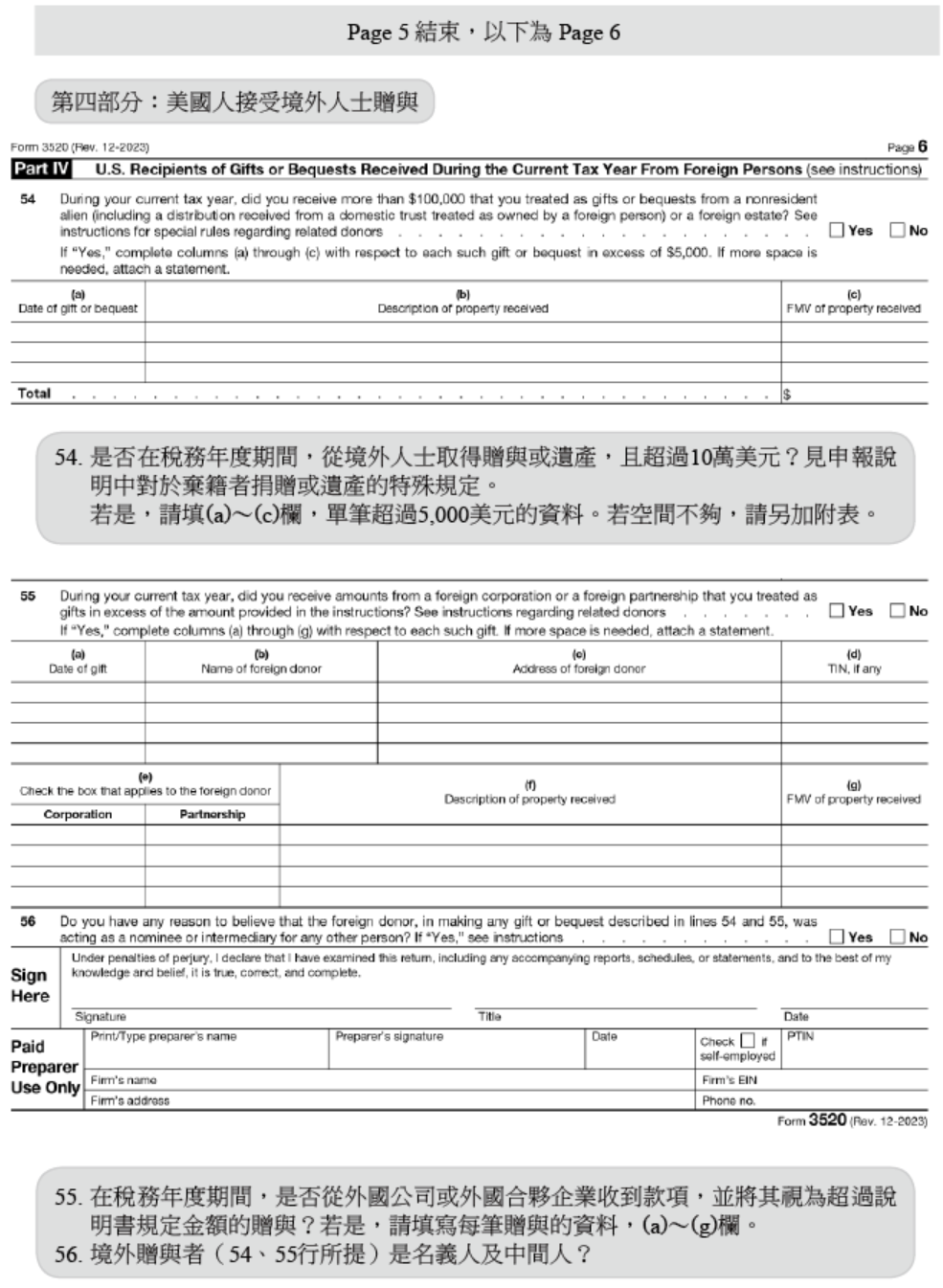

第四部分── 美國人在現行稅務年度,收到外國個人的贈與或遺產

Part IV—U.S. Recipients of Gifts or Bequests Received During the Current Tax Year From Foreign Persons

註:如果未能及時申報應申報的外國贈與(根據第 6039F 條),IRS 可能會確定該贈與的稅額及可能的罰款。

由外國個人捐助給本國或境外信託的資產,且該信託有美國受益人,則這些美國受益人不需在第四部分申報這些資產捐助,除非這些受益人被視為在資產移轉的年度裡收到該捐贈。例如,根據 678 條款,美國受益人是這個信託某部分資產的擁有人,則必須在第四部分申報這項分配。

一個不被視為另一人所擁有的國內信託,則需要在第四部分申報收到外國個人的捐贈;而被視為一外國個人所擁有的國內信託,則不需要申報此部分的捐贈。但是,美國受益人應該要在第四部分申報他收到來自外國人贈與的信託之分配,而非申報在第三部分的美國受益人分配。

Note: If you fail to timely report foreign gifts that should be reported under section 6039F, the IRS may determine the income tax consequences of the receipt of such gift, and penalties may be imposed. See Penalties, earlier.

Contributions of property by foreign persons to domestic or foreign trusts that have U.S. beneficiaries are not reportable by those beneficiaries in Part IV unless they are treated as receiving the contribution in the year of the transfer. For example, if the U.S. beneficiary is treated as an owner of that portion of the trust under section 678, then the contribution must be reported by such U.S. beneficiary in Part IV).

A domestic trust that is not treated as owned by another person is required to report the receipt of a contribution to the trust from a foreign person as a gift in Part IV.

A domestic trust that is treated as owned by a foreign person is not required to report the receipt of a contribution to the trust from a foreign person. However, a U.S. person should report the receipt of a distribution from a domestic trust that is treated as owned by a foreign person as a gift from a foreign person in Part IV, rather than as a distribution to a U.S. person in Part III.

第 54 行

為計算門檻金額(10 萬美元),您務必加總不同的非居住外國人和外國遺產的贈與,如果您知道(或有理由知道)那些個人彼此之間有關係(定義見先前提及的「有關係個人」),或其中一位替另外一位作為被提名人或中間人。

舉例來說,如果您從非居住外國人 A 收到一筆 75,000 美元的贈與,以及從非居住外國人 B 收到 4 萬美元的贈與,而您知道 A 和 B 是有關係的,那麼您務必回答「是」,並且在 (a)~(c) 欄內填入每項贈與。

如果您回答「是」,也沒有收到超過 5,000 美元的贈與或遺產,請不要填寫 (a)~(c) 欄,而是在第 1 行的 (b) 欄中填入:「沒有超過 5,000 美元的贈與或遺產。」

To calculate the threshold amount ($100,000), you must aggregate gifts from different foreign nonresident aliens and foreign estates if you know, or have reason to know, that those persons are related to each other or if one is acting as a nominee or intermediary for the other. See Related Person, earlier.

For example, if you receive a gift of $75,000 from nonresident alien individual A and a gift of $40,000 from nonresident alien individual B, and you know that A and B are related, you must answer “Yes” and complete columns (a) through (c) for each gift.

However, if you answered “Yes” but none of the individual gifts or bequests received exceeds $5,000, do not complete columns (a) through (c). Instead, enter in column (b) of the first line, “No gifts or bequests exceed $5,000.”

第 55 行

如果在本稅務年度內,您自下列任一來源取得的金額合計超過第6039F條規定的門檻金額,且將該等金額視為贈與,請勾選「是」:

- 外國公司。

- 外國合夥企業。

- 您已知或有理由知悉,與該等外國公司或外國合夥企業具關係之任何外國人士。

舉例來說,如果您採用 2023 曆年制來申報,從外國公司 X 收到了 8,000 美元,並將其當作是贈與;另外從非居住外國人 A 收到了 1 萬美元,也將其當作是贈與;而您也知道 A 一人擁有 X 公司,那麼您務必在 (a)~(g) 欄中填入每一項贈與。

Check “Yes” if you received aggregate amounts in excess of the section 6039F threshold amount during the current tax year that you treated as gifts from any of the following.

- Foreign corporations.

- Foreign partnerships.

- Any foreign persons that you know or have reason to know that are related to such foreign corporations or foreign partnerships.

For example, if you, a calendar-year taxpayer during 2023, received $8,000 from foreign corporation X that you treated as a gift, and $10,000 that you received from nonresident alien A that you treated as a gift, and you know that X is wholly owned by A, you must complete columns (a) through (g) for each gift.

註:來自外國公司或外國合夥企業的贈與,根據 672(f)(4) 條款規定,可能會被美國國稅局重新定義其性質。

Note: Gifts from foreign corporations or foreign partnerships are subject to recharacterization by the IRS under section 672(f)(4).

第 56 行

如果您有任何理由相信,在第 54 行或第 55 行所述的任何贈與或遺贈中,外國贈與人係以他人名義行事,或僅作為他人的代理人或中介人,請勾選「是」。若該申報之外國贈與人實際上是代表外國公司或外國合夥企業行事,請另附說明,載明最終外國贈與人的姓名、地址、稅籍編號(如有),以及其為公司或合夥企業。

如果最終捐贈人是境外信託,請把收到的總額當作來自境外信託的分配,並且完成第三部分。

Check “Yes” if you have any reason to believe that the foreign donor, in making any gift or bequest described in lines 54 and 55, was acting as a nominee or intermediary for any other person. If the ultimate donor on whose behalf the reporting donor is acting is a foreign corporation or foreign partnership, attach an explanation including the ultimate foreign donor’s name, address, TIN (if any) and whether it is a corporation or partnership.

If the ultimate donor is a foreign trust, treat the amount received as a distribution from a foreign trust and complete Part III.