專業叢書

Estate Planning by U.S. Trust 美國報稅與海外財產揭露(英文部分)

Appendices

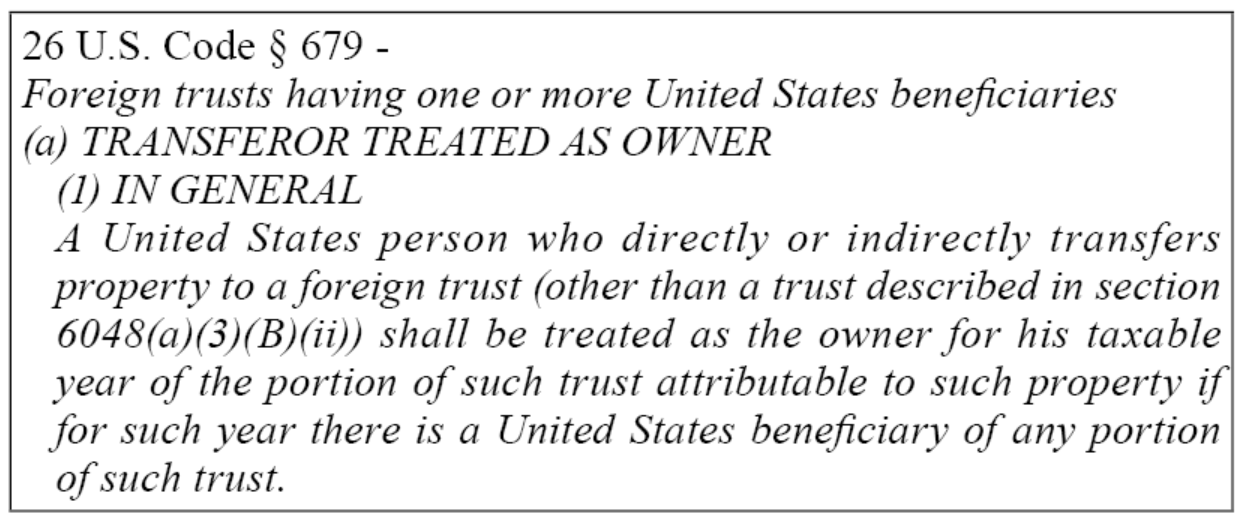

Section E: 26 U.S. Code § 679 Discussion

Case Study: A non-U.S. person established a foreign non-grantor trust and then becomes a U.S. tax resident.

Mr. Wang, a non-U.S. person, has placed US$100,000 per year to a foreign non-grantor trust since 2000. The beneficiaries of this trust are Mr. Wang’s wife and children, both of whom are U.S. tax residents. In 2024, Mr. Wang becomes a U.S. tax resident and it triggers following questions: Whether the trust is subject to U.S. federal income tax because of status change of Mr. Wang? What portion of the trust assets will be subject to U.S. income tax? What is the treatment of the undistributed net income (UNI) accumulated in a foreign irrevocable trust? Will there be any U.S. transfer tax issues?

A trust is recognized a grantor trust because the grantor retains certain powers over the trust assets. However, under U.S. Code § 679, if a U.S. grantor transferred assets into a foreign trust and there’s a U.S. beneficiary, no matter what powers the grantor retains over the trust assets, the grantor shall be treated as the owner for his or her taxable year of the portion of the trust and be subject to U.S. federal income tax.

26 U.S. Code § 679(a)(4) Discussion

For U.S. income tax purposes, foreign trusts with U.S. beneficiaries are taxed at a significantly higher rate than domestic trusts with U.S. beneficiaries. Foreign trusts are trusts that fail either the court test, the control test or both the court and control tests.

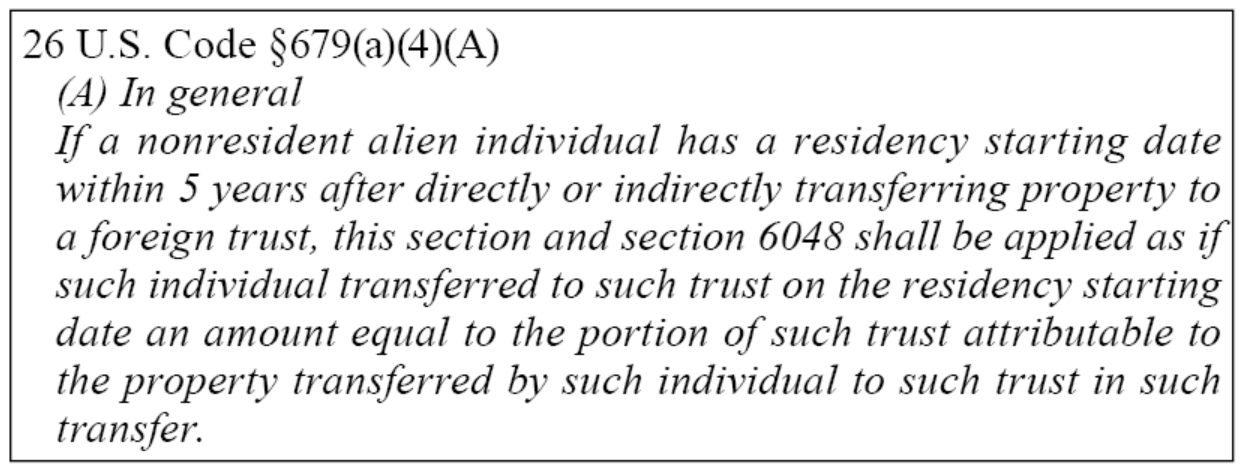

26 U.S. Code §679(a)(4)(A) Excerpt and Case Study

26 U.S. Code §679(a)(4), which was added in 1996, extended §679. Originally, §679 was applied only if the grantor was a U.S. tax resident. After the 1996 Act was enacted, a five-year retroactive period was made to prevent taxpayers from avoiding U.S. income tax through tax planning.

A U.S. person who is deemed to be the owner of a foreign trust will be subject to U.S. income tax each year on the portion of income derived from the portion of the trust’s assets. In Mr. Wang’s case, he shall be treated as the owner of the portion of the trust attributable to property transferred after he becomes a U.S. person in 2024. However, after the §679(a)(4) was added, any income derived from the trust assets which he transferred within five years (i.e., 2019~2023) would attribute to Mr. Wang, which would be subject to U.S. income tax.

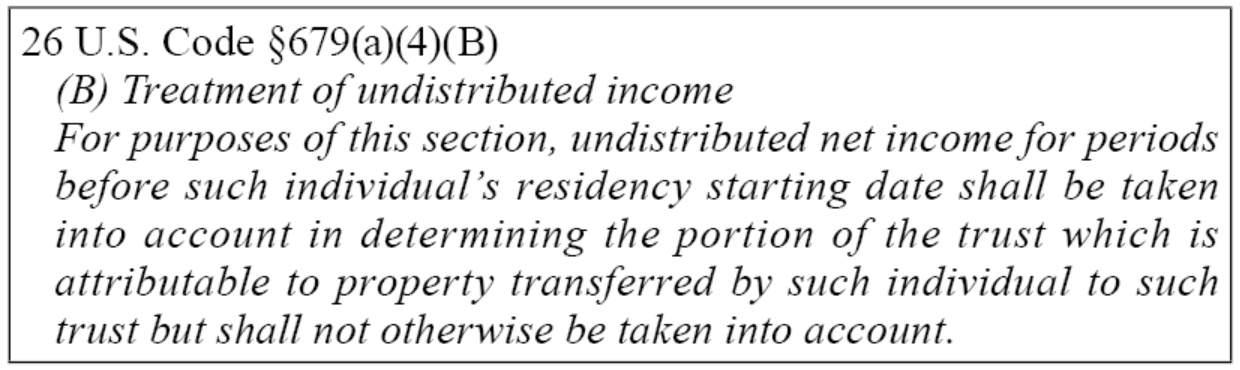

26 U.S. Code §679(a)(4)(B) Excerpt and Case Study

If there’s any UNI generated by the assets which the grantor transferred to the trust within five years before he or she becomes a U.S. person, it is subject to income tax to the grantor.

In this case, Mr. Wang continuously transferred assets to the trust during 2019 to 2023. We assume those assets generate US$10,000 income every year and all the income accumulated in the trust. Therefore, there’s US$50,000 UNI in 2024 when the grantor becomes a US person.

Conclusion:

In this scenario, Mr. Wang becomes a U.S. tax resident in 2024, the portion of the trust that he is deemed as owner is US$550,000 (including US$500,000, he transferred into the trust from 2019 to 2023 and the UNI US$50,000 generated from pervious assets). Mr. Wang must pay income tax for UNI according to §679(a)(4)(B) when he becomes U.S. person. And rest of the assets is subject to income tax in the future.